Options Margin Requirements

Options Margin Overview

US Options Margin Requirements

For residents of Europe trading options:

- Rules-based margin

- Portfolio margin

The complete margin requirement details are listed in the sections below.

The following calculations apply only to Margin, IRA Margin and Cash or IRA Cash. See our Portfolio Margin section for US Options requirements in a Portfolio Margin account.

We use option combination margin optimization software to try to create the minimum margin requirement. However, due to the system requirements required to determine the optimal solution, we cannot always guarantee the optimal combination in all cases. Please note that we do not support option exercises, assignments or deliveries which may result in an account being non-compliant with margin requirements. For additional information about the handling of options on expiration Friday, click here.

Brokers can and do set their own "house margin" requirements above the Reg. T or statutory minimum. For option spreads in VIX securities, we may charge an additional minimum house margin requirement of $150. For option positions that meet the definition of a "universal" spread under CBOE Rule 12.3(a)(5), we may charge an additional house requirement of 102% of the net maximum market loss associated with the spread (i.e., net long option position price – net short option position price * 102%), if greater than the statutory requirement.

Option Strategies

The following tables show option margin requirements for each type of margin combination.

Note:

These formulas make use of the functions Maximum (x, y, ..), Minimum (x, y, ..) and If (x, y, z). The Maximum function returns the greatest value of all parameters separated by commas within the paranthesis. As an example, Maximum (500, 2000, 1500) would return the value 2000. The Minimum function returns the least value of all parameters separated by commas within the paranthesis. As an example, Minimum (500, 2000, 1500) would return the value of 500. The If function checks a condition and if true uses formula y and if false formula z. As an example If (20 < 0, 30, 60) would return the value 60.

Note: Clients must have an account net liquidation value of at least 2,000 USD to establish or increase an existing uncovered options position.

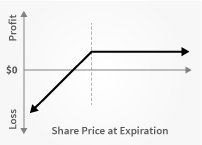

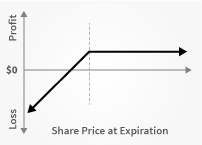

Long Call or Put

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Initial |

| IRA Margin | Same as Margin Account |

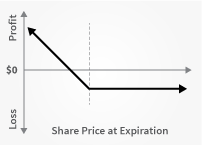

Short Naked Call

| Margin | |

| Initial/RegT End of Day Margin |

Stock Options 1 Call Price + Maximum ((20% 2 * Underlying Price - Out of the Money Amount), (10% * Underlying Price)) Index Options 1 Call Price + Maximum ((15% 3 * Underlying Price - Out of the Money Amount), (10% * Underlying Price)) World Currency Options 1 Call Price + Maximum ((4% 2 * Underlying Price - Out of the Money Amount), (0.75% * Underlying Price)) Cash Basket Option 1 In the Money Amount |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Cash Account |

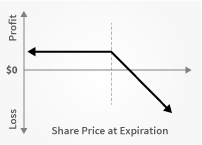

Short Naked Put

| Margin | |

| Initial/RegT End of Day Margin |

Stock Options 1 Put Price + Maximum ((20% 2 * Underlying Price - Out of the Money Amount), (10% * Strike Price)) Index Options 1 Put Price + Maximum ((15% 3 * Underlying Price - Out of the Money Amount), (10% * Strike Price)) World Currency Options 1 Put Price + Maximum ((4% 2 * Underlying Price - Out of the Money Amount), (0.75% * Underlying Price)) Cash Basket Option 1 In the Money Amount |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Put Strike Price |

| IRA Margin | Same as Cash Account |

Covered Calls

Short an option with an equity position held to cover full exercise upon assignment of the option contract.

| Margin | |

| Initial/RegT End of Day Margin | Max(Call Value, Long Stock Initial Margin) |

| Maintenance Margin | MAX[In-the-money amount + Margin(long stock evaluated at min(mark price, strike(short call))), min(stock value, max(call value, long stock margin))] |

| Cash or IRA Cash | Stock paid in full or None |

| IRA Margin | Stock paid in full or None |

Covered Puts

Short an option with an equity position held to cover full exercise upon assignment of the option contract.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Amount |

| Maintenance Margin | Initial Stock Margin Requirement + In the Money Amount |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Call Spread

A long and short position of equal number of calls on the same underlying (and same multiplier) if the long position expires on or after the short position.

| Margin | |

| Initial/RegT End of Day Margin | Maximum (Strike Long Call - Strike Short Call, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Initial if both options are European-style cash-settled Otherwise, N/A. |

| IRA Margin | Same as Margin Account |

Put Spread

A long and short position of equal number of puts on the same underlying (and same multiplier) if the long position expires on or after the short position.

| Margin | |

| Initial/RegT End of Day Margin | Maximum (Short Put Strike - Long Put Strike, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Margin Account (Both options must be European style cash settled) Short Put Strike Price (American style options) |

| IRA Margin | Same as Margin Account |

Collar

Long put and long underlying with short call. Put and call must have same expiration date, same underlying (and same multiplier), and put exercise price must be lower than call exercise price.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Call Amount Equity with Loan Value of Long Stock Minimum (Current Market Value, Call Aggregate Exercise Price) |

| Maintenance Margin | Minimum (((10% * Put Exercise Price) + Out of the-Money Put Amount), (25% * Call Exercise Price)) |

| Cash or IRA Cash | None |

| IRA Margin | None |

Long Call and Put

Buy a call and a put.

| Margin | |

| Initial/RegT End of Day Margin | Margined as two long options. |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | Same as Margin Account |

| IRA Margin | Same as Margin Account |

Short Call and Put

Sell a call and a put.

| Margin | |

| Initial/RegT End of Day Margin |

If Initial Margin Short Put > Initial Short Call, then Initial Margin Short Put + Price Short Call else If Initial Margin Short Call >= Initial Short Put, then Initial Margin Short Call + Price Short Put |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Long Butterfly

Two short options of the same series (class, multiplier, strike price, expiration) offset by one long option of the same type (put or call) with a higher strike price and one long option of the same type with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | None Both options must be European-style cash-settled. |

| IRA Margin | Same as Margin Account |

Short Butterfly Put

Two long put options of the same series offset by one short put option with a higher strike price and one short put option with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | MAX(Highest Put Strike - Middle Put Strike, 0) + MAX(Lowest Put Strike - Middle Put Strike, 0) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Short Butterfly Call

Two long call options of the same series offset by one short call option with a higher strike price and one short call option with a lower strike price. All component options must have the same expiration, same underlying, and intervals between exercise prices must be equal.

| Margin | |

| Initial/RegT End of Day Margin | MAX(Middle Call Options Strike - High Call Options Strike, 0) + MAX(Middle Call Options Strike - Lowest Call Option Strike, 0) |

| Maintenance Margin | Must maintain initial margin. |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Long Box Spread

Long call and short put with the same exercise price ("buy side") coupled with a long put and short call with the same exercise price ("sell side"). Buy side exercise price is lower than the sell side exercise price. All component options must have the same expiration, and underlying (multiplier).

| Margin | |

| Initial/RegT End of Day Margin | None |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Margin Account |

Short Box Spread

Long call and short put with the same exercise price ("buy side") coupled with a long put and short call with the same exercise price ("sell side"). Buy side exercise price is higher than the sell side exercise price. All component options must have the same expiration, and underlying (multiplier).

| Margin | |

| Initial/RegT End of Day Margin | MAX(1.02 x cost to close, Long Call Strike – Short Call Strike) |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | N/A |

| IRA Margin | Same as Margin Account |

Conversion

Long put and long underlying with short call. Put and call must have the same expiration date, underlying (multiplier), and exercise price.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement + In the Money Call Amount |

| Maintenance Margin | 10% of the strike price + In the Money Call Amount |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Reverse Conversion

Long call and short underlying with short put. Put and call must have same expiration date, underlying (multiplier), and exercise price.

| Margin | |

| Initial/RegT End of Day Margin | In the Money Put Amount + Initial Stock Margin Requirement |

| Maintenance Margin | In the Money Put Amount + (10% * Strike Price) |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Protective Put

Long Put and Long Underlying.

| Margin | |

| Initial/RegT End of Day Margin | Initial Stock Margin Requirement |

| Maintenance Margin | Minimum (((10% * Put Strike Price) + Put Out of the Money Amount), Long Stock Maintenance Requirement) |

| Cash or IRA Cash | None |

| IRA Margin | None |

Protective Call

Long Call and Short Underlying.

| Margin | |

| Initial/RegT End of Day Margin | Initial Standard Stock Margin Requirement |

| Maintenance Margin | Minimum (((10% * Call Strike Price) + Call Out of the Money Amount), Short Stock Maintenance Requirement) |

| Cash or IRA Cash | N/A |

| IRA Margin | N/A |

Iron Condor

Sell a put, buy put, sell a call, buy a call.

| Margin | |

| Initial/RegT End of Day Margin | Short Put Strike - Long Put Strike |

| Maintenance Margin | Same as Initial |

| Cash or IRA Cash | If all options are European and cash-settled, same as margin account. |

| IRA Margin | Same as Margin Account |

Portfolio Margin

Under SEC-approved Portfolio Margin rules and using our real-time margin system, our customers are able in certain cases to increase their leverage beyond Reg T margin requirements. For decades margin requirements for securities (stocks, options and single stock futures) accounts have been calculated under a Reg T rules-based policy. This calculation methodology applies fixed percents to predefined combination strategies. With Portfolio Margin, margin requirements are determined using a "risk-based" pricing model that calculates the largest potential loss of all positions in a product class or group across a range of underlying prices and volatilities. This model, known as the Theoretical Intermarket Margining System ("TIMS"), is applied each night to U.S. stocks, OCC stock and index options and U.S. single stock futures positions by the federally-chartered Options Clearing Corporation("OCC") and is disseminated by the OCC to participating brokerage firms each night. The minimum margin requirement in a Portfolio Margin account is static during the day because the OCC only disseminates the TIMS parameter requirements once per day.

However, Portfolio Margin compliance is updated by us throughout the day based on the real-time price of the equity positions in the Portfolio Margin account. Please note, at this time, Portfolio Margin is not available for U.S. commodities futures and futures options, U.S. bonds, Mutual Funds, or Forex positions, but U.S. regulatory bodies may consider inclusion of these products at a future date.

Portfolio or risk based margin has been utilized for many years in both commodities and many non-U.S. securities markets, with great success. Dependent upon the composition of the trading account, Portfolio Margin may require a lower margin than that required under Reg T rules, which translates to greater leverage. Trading with greater leverage involves greater risk of loss. There is also the possibility that, given a specific portfolio composed of positions considered as having higher risk, the requirement under Portfolio Margin may be higher than the requirement under Reg T. Part of the reasoning behind the creation of Portfolio Margin is that the margin requirements would more accurately reflect the actual risk of the positions in an account. Thus, it is possible that, in a highly concentrated account, a Portfolio Margin approach may result in higher margin requirements than under Reg T. One of the main goals of Portfolio Margin is to reflect the lower risk inherent in a balanced portfolio of hedged positions. Conversely, Portfolio Margin must assess proportionately larger margin for accounts with positions which represent a concentration in a relatively small number of stocks.

Portfolio Margin Eligibility

Customers must meet the following eligibility requirements to open a Portfolio Margin account:

- An existing account must have at least USD 110,000 (or USD equivalent) in Net Liquidation Value to be eligible to upgrade to a Portfolio Margin account (in addition to being approved for uncovered option trading). Existing customers may apply for a Portfolio Margin account on the Account Type page in Account Management at any time and your account will be upgraded upon approval. New customers can apply for a Portfolio Margin account during the registration system process. It should be noted that if your account drops below USD 100,000 you will be restricted from doing any margin-increasing trades. Therefore if you do not intend to maintain at least USD 100,000 in your account, you should not apply for a Portfolio Margin account.

- New customer accounts requesting Portfolio Margin may take up to 2 business days (under normal business circumstances) to have this capability assigned after initial account approval. It should be noted that if your account is subsequently funded with less than USD 100,000 in Net Liquidation Value (or USD equivalent), you will be restricted from doing any margin-increasing trades until the Net Liquidation Value exceeds USD 100,000. Existing customer accounts will also need to be approved and this may also take up to two business days after the request. Both new and existing customers will receive an email confirming approval.

- Those institutions who wish to execute some trades away from us and use us as a prime broker will be required to maintain at least USD 6,000,000 (or USD equivalent).

- Customers in Canada are not eligible for Portfolio Margin accounts due to IDA restrictions. In addition, all Canadian stock, stock options, index options, European stock, and Asian stock positions will be calculated under standard rules-based margin rules so Portfolio Margin will not be available for these products.

- Non-U.S. Omnibus Broker (Long Position/Short Position) accounts are not eligible for Portfolio Margin accounts.

- Accounts reporting equity below the $100,000 minimum will be subject to a margin surcharge, the effect of which will be to gradually transition the account to margin levels approximating those of the Reg. T methodology as equity continues to decline.

Portfolio Margin Mechanics

Under Portfolio Margin, trading accounts are broken into three component groups: Class groups, which are all positions with the same underlying; Product groups, which are closely related classes; and Portfolio groups, which are closely related products. Examples of classes would include IBM, SPX, and OEX. A product example would be a Broad Based Index composed of SPX, OEX, etc. A portfolio could include such products as Broad Based Indices, Growth Indices, Small Cap Indices, and FINRA Indices.

The portfolio margin calculation begins at the lowest level, the class. All positions with the same class are grouped and stressed (underlying price and implied volatility are changed) together with the following parameters:

- A standardized stress of the underlying.

- For stock, equity options, narrow based indices and single stock futures, the stress parameter is plus or minus 15%, with eight other points within that range.

- For U.S. market small caps and FINRA market indices the stress parameter is plus 10%, minus 10% as well as eight other points in-between.

- For Broad Based Indices and Growth indices the stress parameter is plus 6%, minus 8% as well as eight other points in-between.

- A market-based stress of the underlying based on historical moves in Bloomberg pricing data.

- For Broad Based Indices the implied volatility factor is increased 75% and decreased by 75%.

- For all other classes, the implied volatility for each options class is increased by 150% and decreased by 150%

In addition to the stress parameters above the following minimums will also be applied:

- Classes with large single concentrations will have a margin requirement of 30% applied to the concentrated position.

- A $0.375 multiplied by the index per contract minimum is computed.

- The same special margin requirements for OTCBB, Pink Sheet and low cap stocks that apply under Reg T, will still apply under Portfolio Margin.

- Initial margin will be 110% of Maintenance Margin.

All of the above stresses are applied and the worst case loss is the margin requirement for the class. Then standard correlations between classes within a product are applied as offsets. As an example, within the Broad Based Index product 90% offset is allowed between SPX and OEX. Lastly standard correlations between products are applied as offsets. An example would be a 50% offset between Broad Based Indices and Small Cap Indices. For stocks and Single Stock Futures offsets are only allowed within a class and not between products and portfolios. After all the offsets are taken into account all the worst case losses are combined and this number is the margin requirement for the account. For a complete list of products and offsets, see the Appendix-Product Groups and Stress Parameters section at the end of this document.

Our real-time, intra-day margining system enables us to apply the Day Trading Margin Rules to Portfolio Margin accounts based on real-time equity, so Pattern Day Trading Accounts will always be able to trade based on their full, real-time buying power.

Because of the complexity of Portfolio Margin calculations it would be extremely difficult to calculate margin requirements manually. We encourage those interested in Portfolio Margin to use our TWS Portfolio Margin Demo to understand the impact of Portfolio Margin requirement under different scenarios.

Click here for the OCC's published list of Product Groups and Offset Parameters.

Additional US Margin Requirements

For Residents of Europe:

Use the following links to view other margin requirements:

You can change your location setting by clicking here

Disclosures

- IBKR house margin requirements may be greater than rule-based margin.